Basics

Understanding P2P lending: the basics for retail investors

How P2P investing works, where the return comes from and what risks sit behind it — a sober primer to get started.

P2P investing sounds simple: you lend your money through a platform to many borrowers and earn interest. Behind that simplicity sits a market with its own mechanics, its own players — and its own risks.

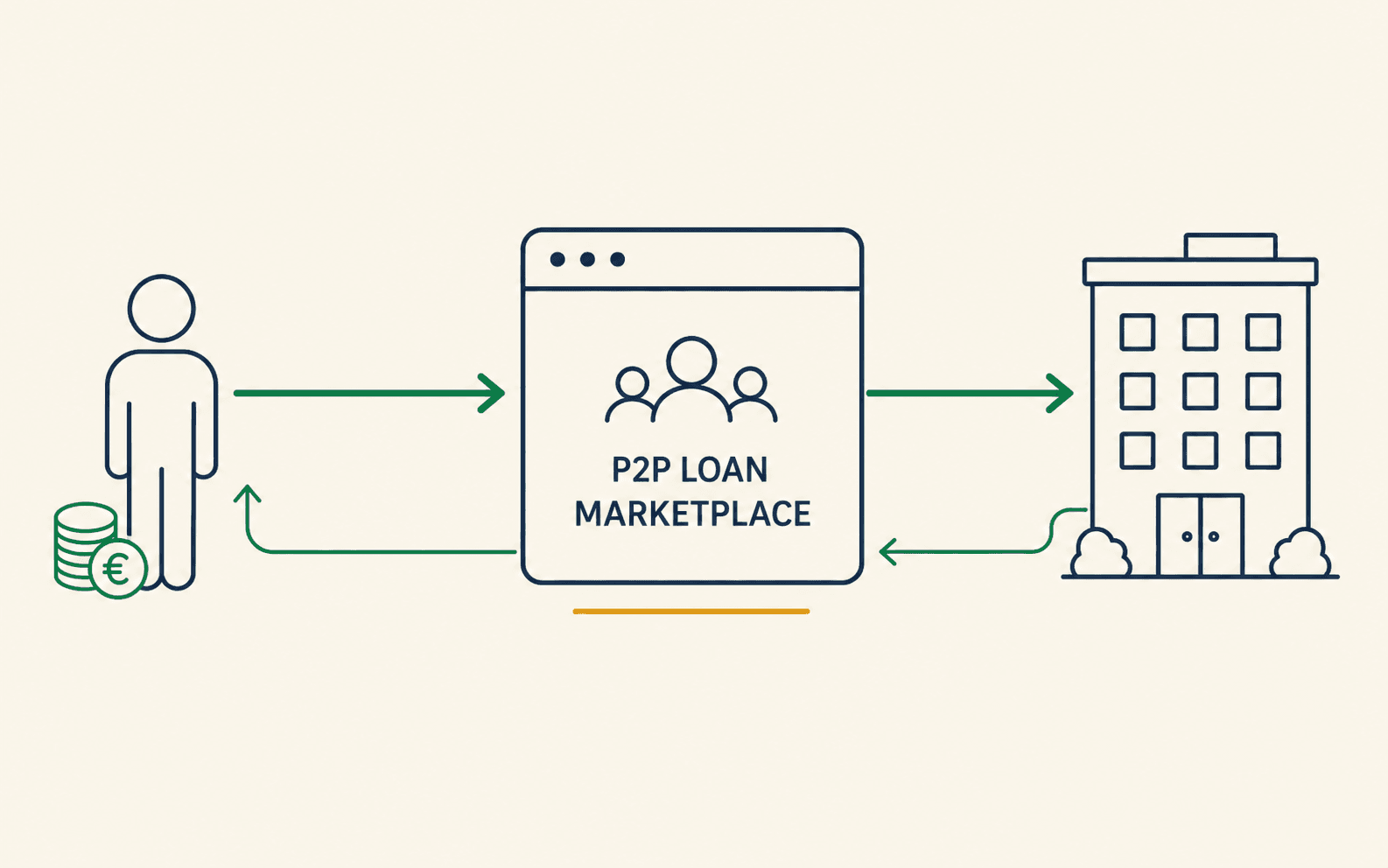

How P2P loans work

A P2P platform connects capital providers (you) with borrowers. You invest small amounts across many loans rather than funding one large loan alone. The platform handles credit checks, servicing and collections — for a fee, and without being liable for defaults itself.

The most important rule first: the platform is an intermediary, not a guarantor. You carry the credit risk.

Where the return comes from

The advertised interest is a risk premium. Higher returns mean higher default risk — not superior terms. Realistic net returns, after defaults and fees, are usually well below the gross headline numbers.

The central risk

No deposit insurance

P2P loans are not a savings deposit. There is no statutory deposit insurance. In the worst case you can lose your invested capital entirely — so diversify broadly and only invest money whose loss you can absorb.

Once you've internalised that, P2P loans can serve as a small, deliberately risky satellite within an otherwise broadly diversified portfolio — no more, but no less. How to spread that satellite across several platforms and loan types — with model portfolios by investment amount — is covered in our guide P2P Lending Diversification.

Frequently asked questions

What are P2P loans?

With P2P (peer-to-peer) loans, retail investors fund loans to individuals or businesses through an online platform and earn interest in return. The platform intermediates but takes on no default risk itself.

Are P2P loans protected by deposit insurance?

No. Unlike a savings account, P2P investments are not covered by any statutory deposit insurance. Individual loans can default down to total loss.